iGaming Market 2026: Modular Platforms, Regulatory Fragmentation, and ‘Build Once, Localize Everywhere’ Setup

The 2026 iGaming market rewards operators who treat regulation as configuration, not code. US online casino revenue reached $10.73 billion in 2025, up 27.6%, but only seven states permit it, with Maine positioned to become the eighth. Each state sets its own KYC, responsible gambling, deposit limits, and reporting rules. A single monolithic build cannot satisfy that fragmentation without costly rework per launch.

NuxGame approaches this market through modular platform components and jurisdiction packs that localize compliance logic while reusing one core. This article maps the reference architecture, data residency choices, and certification sequencing that keep multi-state expansion affordable for B2C brands.

Key Points

The iGaming Market Map: Concentration and Fragmentation

The global online gambling market is expected to grow from about $88 billion in 2025 toward $97.7 billion in 2026. Longer term, the gambling market is projected to reach $202.8 billion by 2033, an 11.0% CAGR. That growth of the online gambling sector frames the 2025 to 2034 window most forecasts model. Sports betting holds the larger revenue share, while online casino content drives the steeper market growth.

The U.S. picture is narrower and more concentrated. Only eight states license real-money online casino play and broader online gaming, with figures from the American Gaming Association showing iGaming revenue up 27.6% to $10.73 billion in 2025. Three markets hold close to 90% of that online casino market. In New Jersey and Pennsylvania, iGaming revenue now exceeds traditional casino revenue.

Several forces drive current market growth and reshape market trends:

- Wider adoption of smartphones and rising internet penetration move demand into mobile gambling and mobile sports betting.

- Convenience and accessibility on phones steadily widen the customer base.

- Technology advancement in live dealers and immersive gaming experiences raise session value.

- Cross-sell from online betting into online casino games like blackjack matures state by state.

| Vertical | 2025 US status | Growth signal | Architecture pressure |

|---|---|---|---|

| Online casino | 8 states licensed | +27.6% YoY revenue | High: per-state game certification |

| Sports betting | ~39 states live | Record handle, higher hold | Medium: odds, in-play latency |

| Online poker | Few states, shared liquidity | Niche, interstate compacts | High: cross-state player pooling |

Sports betting expansion feeds casino conversion later, so timing matters in each new market. Brands that launched online sports betting in 2019 to 2021 are now seeing that cross-sell mature. The delayed effect shapes where the next dollar of net gaming revenue actually appears.

Why Fragmentation Breaks the Single-Stack Approach

No federal statute governs regulated online gambling in the US, so each state writes its own gambling regulations. A slot catalog, payout speed, or bonus mechanic that clears one regulator may be banned one border over. Pennsylvania, New Jersey, Michigan, and five other states each run a separate licensing body. Most treat online casino and sports betting as distinct risk categories, which sets the market dynamics for multi-state coverage.

A monolithic platform encodes one state’s assumptions into shared logic. When the next jurisdiction demands different limits or reporting, engineers patch the core and risk regressions across markets. The result is slow launches, brittle releases, and rising QA cost per market.

These obligations vary independently across jurisdictions:

- Identity and age checks tied to state databases and physical-presence verification.

- Responsible gambling tools such as deposit caps, reality checks, and self-exclusion registers.

- Reporting cadence and format for revenue, taxation, and suspicious-activity filings.

- Approved game types and permitted bet mechanics, which differ by regulator.

Geolocation enforces the border that software, not paperwork, polices. Each state integration adds its own geofencing tolerances and database hooks. Within that perimeter, every online gambling activity is logged for audit; offshore gambling sites and unlicensed forms of gambling sit outside it, so those gambling activities never reach state systems. The online gambling industry treats that boundary, not the license document, as the real compliance edge.

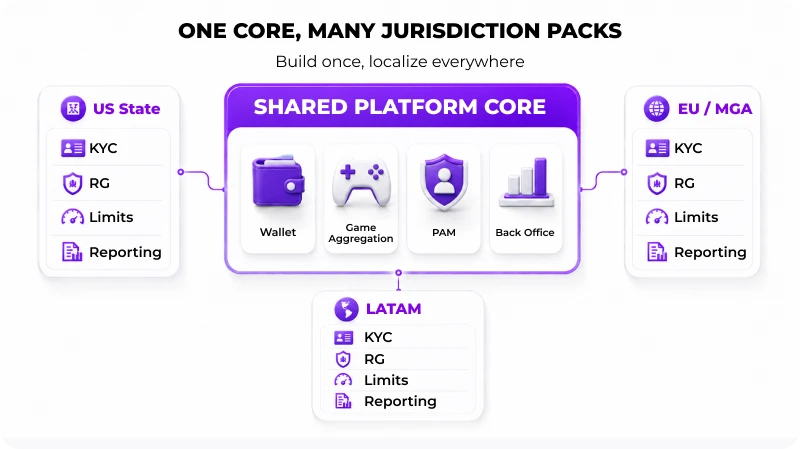

Modular Platform Architecture: Build Once, Localize Everywhere

A modular approach separates the shared core from per-market behavior in online gambling platforms. The wallet, game aggregation layer, player account management, and back office stay common. Regulation, limits, and reporting move into swappable configuration that loads per jurisdiction. This mirrors composable architecture principles that Gartner describes for adaptable systems; the iGaming industry is consolidating onto cores built this way.

The NuxGame platform structures this split so a new market becomes a configuration exercise, not a rebuild. As a B2B platform provider, it lets teams reuse one certified core and attach the rules a regulator demands. The same core serves sportsbook and casino verticals through shared betting platforms, cutting vendor connections and launch time.

For operators, expansion should not feel like rebuilding the business at every border. The goal is to keep the platform core stable while local rules move into controlled configuration. That gives teams a cleaner launch path, fewer duplicated costs, and more room to focus on product growth instead of repeating the same compliance work.

Denis Kosinsky

Chief Product Officer at NuxGame

Jurisdiction Packs: KYC, RG, Limits, and Reporting

A jurisdiction pack bundles everything that differs by state into one versioned unit. It carries KYC provider routing, RG defaults, transaction limits, tax logic, and report templates. When a regulator updates a rule, the pack version changes, not the platform core.

| Pack component | What it controls | Why it stays isolated |

|---|---|---|

| KYC routing | Verification provider, data fields, retry logic | Provider acceptance varies by state |

| RG ruleset | Limits, cooldowns, self-exclusion sync | Each regulator mandates different tools |

| Limit engine | Deposit, loss, session, wager caps | Caps and defaults are state-specific |

| Reporting | Format, cadence, taxable base | Filing schemas differ per authority |

Wallet, Aggregation, and Session Continuity

The wallet muststay consistent while gaming content streams from many studios through one aggregation layer. Whether a sports betting platform or a table-game front end, both draw on that single balance. Production setups typically hold wallet-sync targets under 300 ms and platform uptime objectives at 99.9% or higher. GLI-19 requires that an interrupted game resumes correctly after a dropped connection or platform restart. The session layer must persist unresolved rounds and replay the RNG outcome on reconnection, protecting both player balance and audit integrity.

Player Data Sovereignty and Residency Strategy

Where player records physically live is an architectural and legal decision, not an afterthought. US state regulators expect auditable local access, and in a key market such as Pennsylvania that expectation is explicit. The digital infrastructure behind a growing player base must respect those lines. A residency strategy then defines which records stay in-region and which replicate.

Latency and sovereignty pull in opposite directions and need deliberate balancing. Centralizing data simplifies operations but adds round-trip delay for distant players. Regional placement using data residency controls from AWS keeps records in-jurisdiction, while edge delivery via data localization options from Cloudflare trims latency and absorbs traffic spikes.

A practical residency model separates data by sensitivity and obligation:

- Identity and KYC records: stored in-region, encrypted, with restricted regulator access paths.

- Transaction and wager logs: retained per local reporting and audit retention rules.

- Behavioral and session data: cached at the edge for user experience, never as the system of record.

Compliance Engineering: GLI-19, PCI DSS, and Reporting

GLI-19 sets the technical baseline for interactive gaming systems, covering RNG strength, game fairness, and transaction logging. The standard, published by bodies including the GCGRA interactive gaming systems authority, dictates how incomplete games resolve and how audit trails capture every event. Certification is not a label; it forces specific logging granularity and failure-recovery behavior into the architecture. Inadequate transaction logging is a common cause of failed submissions.

Payment security adds a parallel, non-negotiable track. Today, assessments run against PCI DSS v4.0.1, the current version maintained by the PCI Security Standards Council. The 51 future-dated controls became mandatory on 31 March 2025, with no remaining grace period.

Two requirements reshape the payment page directly, while a third expands authentication coverage:

| Requirement | Obligation | System impact |

|---|---|---|

| 6.4.3 | Inventory and integrity-check all payment-page scripts | Script allowlisting and tamper detection |

| 11.6.1 | Detect unauthorized changes to payment pages | Weekly change/tamper monitoring |

| 8.3.1 | MFA for all access into the cardholder data environment | Expanded authentication coverage |

These controls turn compliance from an annual event into continuous monitoring. Reporting obligations then layer on top: revenue filings, RG audit logs, and suspicious-activity records each follow a jurisdiction-specific schema and cadence.

Regional Responsible Gambling Variations

Responsible gambling rules diverge more than any other compliance layer across markets. The UK enforces strict affordability and intervention duties under the licensing conditions and codes maintained by the Gambling Commission. Germany’s framework centralizes cross-operator deposit limits and self-exclusion through a national system. US states each define their own caps, cooldowns, and exclusion registers, with no shared standard.

A configuration-driven RG layer absorbs this variance without forking the platform. Defaults, intervention triggers, and exclusion sync all live inside the jurisdiction pack. Licensed under frameworks such as the Malta Gaming Authority regime, EU-facing brands attach a different pack. The same approach extends to a new market like Latin America as the global market fragments, so one iGaming business can run several regions from a single core. Across the global iGaming sector, that reuse is what keeps multi-region compliance affordable.

Compliance teams should treat RG triggers as testable rules, not policy text:

- Deposit and loss caps: enforced server-side, versioned per market.

- Reality checks and session reminders: interval values set by regulator.

- Self-exclusion: synchronized with national or state registers in near real time.

Avoiding Over-Compliance Costs Through Sequencing

Over-compliance is as expensive as non-compliance, and it is avoidable. Certifying separately for each state can mean paying for full testing cycles three to five times. Multi-game platform certification commonly runs $75,000 to $150,000, with RNG testing alone taking four to twelve weeks. Each redundant cycle erodes online gambling revenue and early market share before a launch even matures.

The efficient path certifies to the strictest regulator first. Pennsylvania’s requirements exceed most states, so a Pennsylvania certification covers roughly 90% of New Jersey, Michigan, and West Virginia obligations. The online casino market segment carries the heaviest certification load, so sequencing it first protects margin. State-specific addendum testing, such as geolocation accuracy and database integration, still applies, but core retesting does not.

| Risk | Trigger | Mitigation |

|---|---|---|

| Repeat certification spend | Per-state full retesting | Certify strictest market first |

| Launch delay | Reverse-engineering by labs | Submit full documentation upfront |

| Data exposure | Misplaced residency | Region-locked storage by record type |

| RG audit failure | Hardcoded limits | Config-driven, versioned RG packs |

Technical Snapshot

| Area | Implementation checkpoint | Indicator / dependency |

|---|---|---|

| Platform core | Shared wallet, aggregation, PAM, back office | Uptime objective 99.9%+ |

| Localization | Versioned jurisdiction packs | One core, many markets |

| Session integrity | GLI-19 incomplete-game recovery | RNG replay on reconnection |

| Payments | PCI DSS v4.0.1, controls 6.4.3 / 11.6.1 / 8.3.1 | Script integrity, MFA into CDE |

| Data residency | Region-locked KYC and transaction logs | Edge caching for non-record data |

| Certification | Strictest-market-first sequencing | ~90% reuse across neighbors |

| Wallet sync | Cross-studio balance consistency | Target under 300 ms |

Bottom Line

The 2026 iGaming market is not won by adding states one rebuild at a time. It is won by deciding, once, where regulation lives in the stack. The key players in the gaming industry already run this way. Online gambling operators who push KYC, RG, limits, and reporting into versioned configuration launch faster and reduce certification costs. Gaming operators that hardcode one state’s rules pay for it on every expansion. The decision in front of CTOs and product managers is architectural: a shared certified core with localized packs, or a monolith that fragments under its own jurisdictions. NuxGame exists to make the first option the default path for B2C brands.

Planning a multi-state or multi-region launch and unsure where compliance logic should live? Through its online casino platform, NuxGame gives B2C brands a single certified core, with jurisdiction packs for KYC, responsible gambling, limits, and reporting, plus casino aggregation, wallet synchronization, and back-office configuration. Talk to the NuxGame team to map your reference architecture and certification sequence before you commit engineering budget.